Maritime Market News

News Highlights week: 02 - 2024

Ngày đăng: 12/01/2024 | Lượt xem: 767

GSL starts China-Cambodia-Thailand-Vietnam service

Gold Star Line (GSL) last week introduced a new ‘SXT’ service connecting South China, Cambodia, Thailand and Southern Vietnam.

The Hong Kong-based operator deploys two 1,600 - 1,900 teu ships to operate this weekly service. The 1,645 teu SEA OF LUCK which offered the first sailing on 7 January from Nansha, is joined by the 1,930 teu KANWAY FORTUNE.

The ‘SXT’ loop turns in two weeks calling at Nansha, Dachan Bay, Sihanoukville, Laem Chabang, Bangkok, Cai Mep, Nansha.

GSL's new ‘SXT’ complements the existing ‘CTV’ service, which is offered in partnership with Jin Jiang shipping. This 'CTV' covers Central & South China, Thailand, Cambodia and Southern Vietnam.

Far East - Europe rates spiral on Gaza conflict

Liner disruption in the wake of the Gaza conflict have pushed spot prices on the Far East-Europe route to their highest level in fifteen months.

Rates on the trade jumped to USD 2,694 per teu on Friday, an 80% increase compared to the previous week. Levels have more than tripled since the start of the month.

Operators last saw equivalent rates in the run-up to China’s Golden Week holiday at the start of October 2022.

Spot rates on the Far East to Mediterranean trade also rose by 70% week-on-week to reach a level of USD 3,491 per teu on Friday, also a 15- month high.

Meanwhile, the Shanghai Containerized Freight Index (SCFI) hit 1,760 points on Friday, with all component routes showing a positive weekly improvement, barring the regional Shanghai-Japan and Shanghai-Korea trades.

With the disruption of the war, the SCFI has now risen above 2023’s average of 1,006 points. Carriers may also be benefitting from firming demand, with Chinese exports growing for the first time in six months in November.

Prior to the launch of Hamas’ surprise attack on 7 October, the SCFI had fallen to its lowest level since the outbreak of the COVID virus. However, it had still not fallen below 2019 levels, although carriers point out costs are now significantly higher than before COVID.

Red Sea crisis impact starts to show in Charter Market

The container charter market has started off 2024 in an equally busy way as it ended 2023. Despite a continued influx of newbuilding tonnage of all types, demand for most sizes of charter market ships, apart from the small ones, remains strong.

The crisis in the Red Sea, with most carriers now avoiding the area, is in part contributing to the market’s brisk activity, with extra tonnage deployed to compensate for the much longer transit times needed via the Cape of Good Hope to connect Asia with any region west of Suez. The question is how long this crisis will last and what full impact that could have on the charter market, should the situation persist in the longer term. Alphaliner is already aware of at least four vessels fixed either as ‘Red Sea traders’ at premium rates or as extra loaders from Asia to Europe. More such fixtures will likely follow in the coming days.

Strong cargo volumes out of Asia are also fueling demand for tonnage, ahead of the Chinese New Year starting in a month from now.

A combination of these factors is resulting in skyrocketing freight rates, particularly between Asia and Europe where the shipment of a Teu container out of China is now rated by the SCFI in excess of USD 2,800, versus only USD 850 in early December.

This being said, 2024 could be another challenging year for the market with around 3.2 M teu of newbuilding capacity expected to hit the water within the next twelve months. Obviously, a persistent crisis in the Red Sea and, to a lesser extent, ongoing problems at the Panama Canal could partly cushion the risk of overcapacity thanks to the demand for extra tonnage they will generate. CII will also continue to help, so will demolition, but yet, cargo demand will need to be very strong across the board to absorb the upcoming newbuild capacities. As a result, Alphaliner remains cautious about the charter market prospects for this new year.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 03 - Oct | 26 - Sep | CHG | |

| $-VND | 26,420 | 26,453 |  33 33 |

| $-EURO | 0.852 | 0.855 | 3 |

| CNY-VND | 3,764 | 3,759 | 5 |

| SCFI | 1,115 | 1,115 | 0 |

| BUNKER PRICES | ||||

| 03 - Oct | 26 - Sep | CHG | ||

| RTM | 380cst | 397 | 418 | 21 |

| LSFO 0.50% | 434 | 463 | 29 |

|

| MGO | 659 | 695 | 36 |

|

|

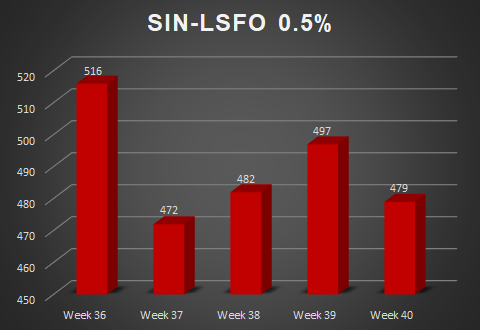

SGP |

380cst | 407 | 424 | 17 |

| LSFO 0.50% | 497 | 497 | 0 |

|

| MGO | 679 | 702 | 23 |

|

Tin nổi bật

-

-

Nghị quyết Hội đồng quản trị ngày 01/10/2025

Ngày 02/10/2025

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025