Maritime Market News

News Highlights week: 03 - 2023

Ngày đăng: 18/01/2023 | Lượt xem: 525

GSL revamps China -Thailand - Northern Vietnam loop

Gold Star Line (GSL) is in the process of revamping its ‘CT3’ service, which was only launched in November to cover Central and South China, Thailand and Northern Vietnam.

ZIM also participates in this service and its uses the same ‘CT3’ brand name.

GSL now expands the ‘CT3’ to include North China and Cambodia at the expense of Xiamen in South China and of the loop’s southbound call at Laem Chabang in Thailand.

Starting with the departure of the 1,762 teu MTT SANDAKAN from Xingang on 14 January, the expanded ‘CT3’ will turn in four weeks instead of its original three weeks.

The loop henceforth will offer weekly calls at Xingang, Dalian, Qingdao, Shanghai, Ningbo, Nansha, Sihanoukville, Bangkok, Laem Chabang, Haiphong, Yantian, Nansha, Xingang. Its uses a fleet of four 1,700 - 1,900 teu ships.

This updated ‘CT3’ allows Gold Star Line to serve Sihanoukville, the main gateway into Cambodia, with its own tonnage. Previously, GSL only covered this port through ad hoc local feeders.

Asia-Europe: 27% of sailings axed in first seven weeks of 2023

The three big carrier alliances plan to skip 27% of their originally scheduled Asia – Europe sailings in the first seven weeks of this year.

Under normal circumstances, the shipping lines’ 18 Far East - North Europe and ten Far East - Med loops should have offered a total of 196 sailings in the period from 1 January to 17 February. This is however not the case.

Based on the observed actual sailings in the first weeks of this year, as well as published forward schedules for the upcoming weeks, it appears that 53 of these planned voyages have been axed due to a lack of cargo demand. This number could still increase if the carriers decide to blank further sailings after the week-long Chinese New Year Holidays, which will start on 21 January.

It has become a general practice for container lines to ‘void’ sailings in the calm weeks after the Chinese New Year. In contrast to this, the weeks before the holidays typically saw a small export rush from China, as cargo is shipped out before the factories close and productions comes to a near standstill.

Despite the fact that some newcomers such as CULines and Allseas have dropped out of the Asia – Europe trades already, the big carriers this year nevertheless reduced the number of westbound departures ahead of the holiday.

Alphaliner counted 69 ships that started a round voyage to North Europe or the Mediterranean in their first Far Eastern load port between 1 and 20 January. Under a ‘normal’ schedule, the number of sailings on alliance loops in this period should have reached 84 westbound departures.

According to preliminary figures from Container Trades Statistics, cargo volumes between Asia and Europe fell by 18.4% in November, following an even bigger drop of 25.9% in October.

The blanking of sailings before the Lunar New Year Holidays now shows that cargo demand out of Asia has not yet recovered.

This represents a 29% reduction in the number of 2M sailings in the first seven weeks of the year. Counting also Asia – Med departures, the 2M offers 24% fewer westbound trips in the Asia – Europe trade. The OCEAN Alliance has made similar efforts, by reducing the number of westbound voyages by 23%. The COSCO-operated Far East – North Europe loop ‘AEU7’ loop (aka OCEAN’s ‘NEU3’) is the worst affected. Its schedule shows only three departures from Xiamen in the first seven weeks, namely on 5 January, 18 January and 8 February.

Our chart on page one illustrates that THE Alliance has been most active carrier group when it comes to limiting the number of sailings from the Far East to Europe.

THEA’s 36% reduction in sailings is partly due to the fact that Hapag Lloyd, HMM, ONE and Yang Ming divert more North Europe to Asia backhaul sailings from the Suez Canal to the Cape of Good Hope route than other carriers. This detour adds two weeks of steaming to the trip and it therefore leads to later vessel arrivals back in China.

The big carriers do not only skip sailings to adjust capacity supply to the lower cargo demand, but also to avoid a further erosion of spot ocean freight rates from China.

So far however, this capacity management has not helped much to lessen the downward pressure on rates. Spot freight rates from Shanghai to North Europe fell slightly to USD 2,040 per feu last week, according to the Shanghai Containerized Freight Index. Spot rates have thus returned to the levels seen in September 2020.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

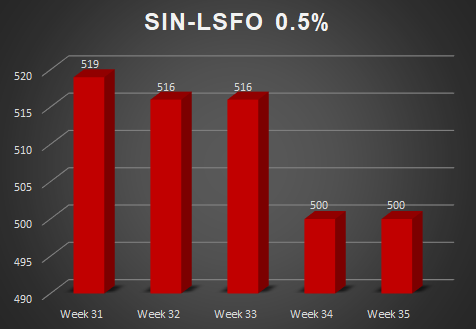

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025