Maritime Market News

News Highlights week: 05 - 2023

Ngày đăng: 02/02/2023 | Lượt xem: 582

Carriers shift tonnage to Middle East and India related loops

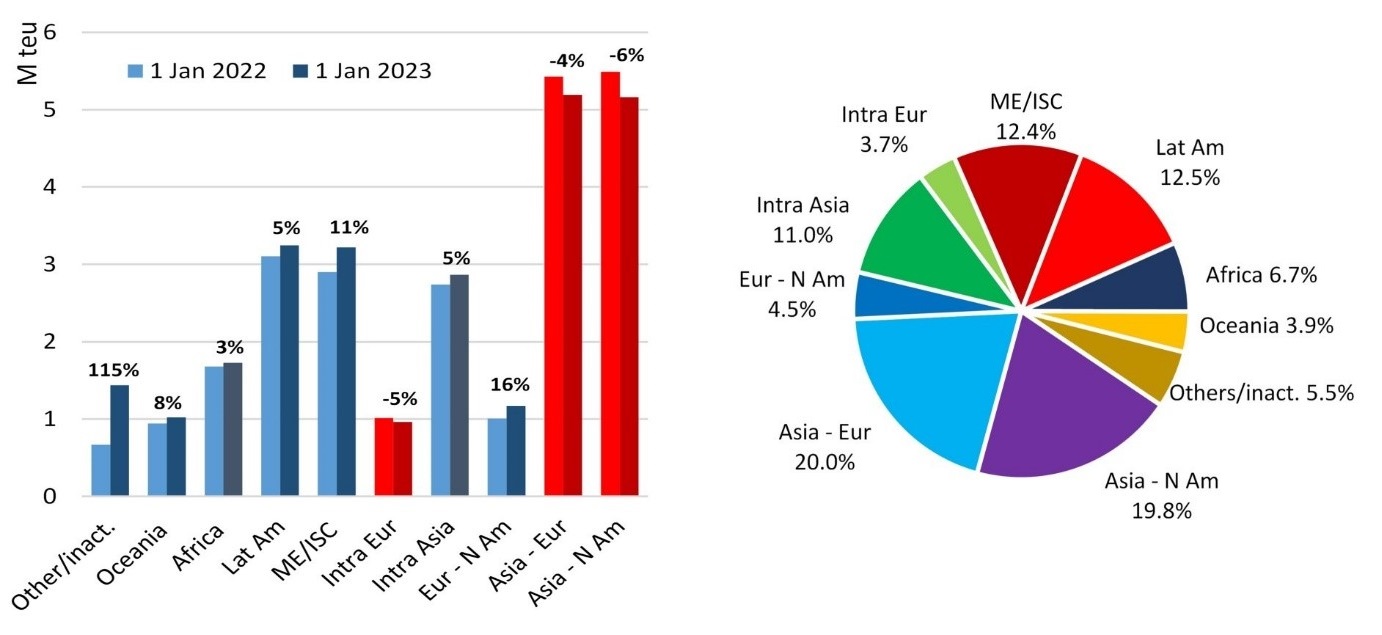

Poor cargo demand in China and falling ocean spot freight rates have led to significant changes in global container fleet deployment. More than 565,000 teu of capacity was withdrawn from the Asia - North America and Asia - Europe trades in 2022. This process is still continuing with Hapag-Lloyd closing down its China - Germany Express service and Ellerman re-deploying ships on the more lucrative Transatlantic trade.

The active container fleet on the Transatlantic increased by an impressive 16.2% in 2022, equivalent to 162,300 additional teu slots. The biggest tonnage shift however has been to Middle East and India related services (+11%), where 320,600 teu of fleet capacity was added last year.

Indian ports are now handling an increasing number of 13,000 - 15,000 teu ships which have been replaced by megamax vessels on the East West trades. The growing interest in Indian traffic was reflected by sister companies COSCO Shipping Lines and OOCL launching a South East Asia - India - US East Coast ‘AWES / ISE’ service in December after closing a China - Vietnam - USEC ‘AWE6 / VCE’ loop.

MSC and Maersk let 2M partnership expire in 2025

The world’s largest and second-largest container shipping lines, MSC and Maersk, last week announced that their ‘2M’ vessel sharing agreement will be discontinued in early 2025.

In a joint statement issued on 25 January, MSC and Maersk said that the two companies had mutually agreed to discontinue the 2M after a period of ten years.

MSC and Maersk jointly stated that much had changed since the two companies signed the ten-year agreement in 2015. The carriers commented: ‘Discontinuing the 2M alliance paves the way for both companies to continue to pursue their individual strategies’.

The break-up of MSC and Maersk will certainly bring about significant changes to the global liner shipping landscape.

Potentially, it could even trigger a re-organization of today’s carrier alliances, as several of the shipping lines involved in the three big groups, 2M, OCEAN and THEA, could reconsider their strategic longterm options.

Next to OCEAN (CMA CGM, COSCO, Evergreen and OOCL) and THEA (Hapag-Lloyd, ONE, HMM and Yang Ming), the 2M Vessel Sharing Agreement is one of today’s global carrier alliances.

Unlike the other two, 2M has always avoided the ‘alliance’ moniker and referred to itself as a Vessel Sharing Agreement. For all intents and purposes though, it can be counted as a carrier alliance. The 2M was set up in 2014 and it became operational in January 2015. Originally, MSC and Maersk had planned to partner with CMA CGM and form a carrier trio, but objections from government regulators put an end to this plan.

Next to the full partners MSC and Maersk, the 2M also cooperated with a small number of other carriers on selected trades. This includes HMM which later became a THEA member, as well as ZIM and SM Line.

Like with all major alliances, the 2M’s scope is limited exclusively to the three main East - West corridors: Firstly Far East - Americas, secondly Far East - Europe / Med and thirdly Europe - North America. Compared to OCEAN and THEA, the 2M is even more limited in scope as it does not cover trades to and from the Middle East.

The 2M partners currently control 33.7% of the global container fleet: MSC stands at 4.63 Mteu / 17.6%, while Maersk has 4.23 Mteu / 16.1%. However, not all of this capacity is deployed under the umbrella of the 2M VSA.

MSC currently only uses 25% of its fleet capacity (1.15 Mteu) in the 2M setup, while Maersk deploys 39% (1.66 Mteu) of its fleet within the partnership’s service network. This results in a 41%-59% split within the 2M. Both carriers operate the remainder of their fleets on independent services or within other regional cooperations.

Since the launch of 2M, both MSC and Maersk have grown massively. MSC’s fleet has almost doubled from 2.54 Mteu in January 2015, while Maersk stood at 2.89 Mteu, almost three years before the takeover of Hamburg Sud.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 05 - Sep | 29 - Aug | CHG | |

| $-VND | 26,510 | 26,502 |  8 8 |

| $-EURO | 0.855 | 0.856 | 1 |

| CNY-VND | 3,754 | 3,754 | 0 |

| SCFI | 1,444 | 1,445 | 1 |

| BUNKER PRICES | ||||

| 05 - Sep | 29 - Aug | CHG | ||

| RTM | 380cst | 391 | 411 | 20 |

| LSFO 0.50% | 452 | 465 | 13 |

|

| MGO | 658 | 650 | 8 |

|

|

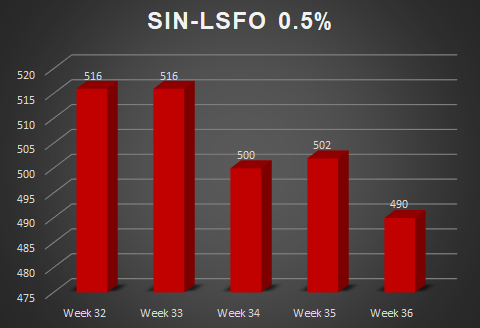

SGP |

380cst | 405 | 412 | 7 |

| LSFO 0.50% | 490 | 502 | 12 |

|

| MGO | 670 | 648 | 22 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025