Maritime Market News

News Highlights week: 08 - 2024

Ngày đăng: 26/02/2024 | Lượt xem: 670

ONE teams up with Wan Hai Lines in Transpacific VSA

Ocean Network Express (ONE) will at the end of April or early May launch a new Vietnam – China – Taiwan – California ‘AP1’ loop which will be jointly operated with Wan Hai Lines.

The new Transpacific Southwest loop will succeed to Wan Hai’s current standalone ‘AA3’ service, which turns in eight weeks calling at Cai Mep, Shekou, Xiamen, Taipei, Ningbo, Shanghai, Los Angeles, Oakland, Shekou, Cai Mep.

Retaking this ‘AA3’ rotation, the new ‘AP1’ will also call at Haiphong and turn in eight weeks. While Wan Hai Lines has confirmed the 56- day fixed round trip schedule, the press release and the Vessel Sharing Agreement (VSA) which was filed with the Federal Maritime Commission (FMC) in Washington, clearly mention that Wan Hai Lines will provide five vessels and ONE two.

The partners have agreed that the ‘AP1’ ships should have a capacity in the size range of approximately 5,500 to 14,000 teu and that the agreement shall have a minimum period of 12 months after becoming effective.

Wan Hai currently deploys two 3,000 teu and two 13,250 teu vessels in the ‘AA3’, but two more ships of 3,013 teu and 13,458 teu respectively are to join the fleet in the first half of March.

The new VSA fuels speculation about Wan Hai Lines possibly becoming a member of THE Alliance at the end of January 2025, when Hapag-Lloyd leaves the alliance to start a new ‘Gemini Cooperation’ with Maersk on the big East West trades.

ONE currently brings in 38.7% of all THE Alliance capacity (equivalent of 1.2 Mteu), while Hapag-Lloyd’s vessels in THE Alliance services have a combined capacity of 817,000 teu (26.2%). The German carrier is the leading tonnage provider on the Transatlantic trade.

For comparison sake: Wan Hai’s fleet of 18 neo-panamaxes (five of which are still under construction) represents a capacity of 242,000 teu

No weakness in sight for charter market

The container charter market remains on a rising trend with Non Operating Owners (NOOs) benefitting from continuously favorable winds.

Despite the Chinese New Year holiday in Asia last week, activity has barely dropped, with demand for most size of vessels remaining brisk across the board.

As the supply of prompt tonnage continues to be tight, especially for larger vessels (4,000 teu and above), charter rates are rising sharply in these sizes, with any new fixture typically concluded at much higher levels than last done deals. Owners meanwhile are trying to obtain the longest possible commitments from charterers, with mixed success though.

In the smaller sizes, particularly below 3,000 teu, charter rates also remain on a positive trend, but most of the gains are achieved on modern, energy-efficient tonnage, with carriers in some cases willing to pay very large premiums compared to more standard units.

The high activity in the market remains mostly driven by the consequences of the situation in the Red Sea, as well as high cargo volumes on some important routes. With a growing number of industry stakeholders banking on an extended period of disruptions in the Red Sea, NOOs can expect a continued strong market in the short term.

Further down the road, overcapacity remains the principal threat for 2024, with the influx of newbuilding tonnage showing no sign of easing.

Meanwhile on the cargo front, freight rates have been on their fourth week of decline on the Asia-Europe route and, as anticipated by Alphaliner, are now also dropping on the so far glittering transpacific.

Meanwhile, North-South trades are a mixed bag, with some routes performing better than others. Finally, oil prices have been going up again in the last days, amid ongoing geopolitical tensions in the Middle East.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 03 - Oct | 26 - Sep | CHG | |

| $-VND | 26,420 | 26,453 |  33 33 |

| $-EURO | 0.852 | 0.855 | 3 |

| CNY-VND | 3,764 | 3,759 | 5 |

| SCFI | 1,115 | 1,115 | 0 |

| BUNKER PRICES | ||||

| 03 - Oct | 26 - Sep | CHG | ||

| RTM | 380cst | 397 | 418 | 21 |

| LSFO 0.50% | 434 | 463 | 29 |

|

| MGO | 659 | 695 | 36 |

|

|

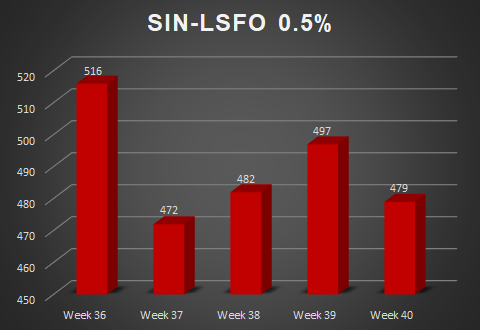

SGP |

380cst | 407 | 424 | 17 |

| LSFO 0.50% | 497 | 497 | 0 |

|

| MGO | 679 | 702 | 23 |

|

Tin nổi bật

-

-

Nghị quyết Hội đồng quản trị ngày 01/10/2025

Ngày 02/10/2025

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025