Maritime Market News

News Highlights week: 09 - 2022

Ngày đăng: 04/03/2022 | Lượt xem: 558

Newbuildings won’t solve ocean capacity crunch before 2023

Carriers and non-operating owners have made 2021 a bumper year for container vessel orders and contracting activity continued through the first two months of 2022. So far, rapidly escalating vessel prices have not yet deterred buyers.

To the contrary, some of the earlier-placed newbuilding contracts of 2021 may very well have been motivated by asset play moves and we have recently seen a number of ship owners - the ones that had bet on rising prices early on - cash in on resales of yet-to-be-delivered tonnage.

Further to this, carriers felt compelled to convert essentially all shipyard options, locked in at 2020 or early 2021 prices, since the deals were just too good to refuse in today’s price-inflated world. A weakening Chinese Yuan and Korean Won, measured against the US Dollar, furthermore should have helped convince shipping lines to place orders last year.

Carriers also used their massive windfall profits, generated on the back of soaring ocean freight rates, to renew their fleets with modern, high-spec tonnage.

With everyone rushing to get ships into the water as soon as possible, early delivery rates are much sought after and carriers have signed a healthy number of container ships at yards hitherto better known for building bulkers, tankers, or roro passenger ferries.

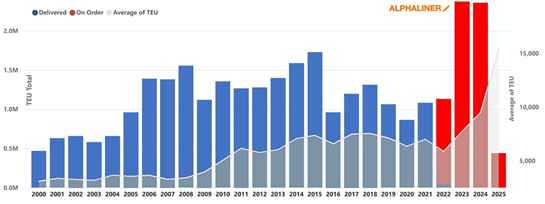

As per February, the global orderbook-to-fleet ratio has crept up to about 25% again. While this is still lightyears away from the ‘crazy’ 65% of 2008, today number relates to a baseline fleet that has more than doubled in size since then to reach well in excess of 25 Mteu.

In absolute terms, the ’confirmed’ orderbook now stands at more than 6.22 Mteu. The actual number will be slightly higher since Alphaliner has excluded a few recent orders placed without formal disclosures that have yet to be verified through industry channels.

Since the uptick in orders only came in mid-2020, when the orderbook-to-fleet ratio was only 9%, newbuilding deliveries this year are forecast at ‘only’ around 1.10 Mteu. This is roughly in line with the average in 2016 - 2021, when annual boxship deliveries oscillated around the 1.00 Mteu mark.

The vast majority of container ships ordered in the recent boom will only join active service in 2023 and 2024, as illustrated in the graph below

Based on today’s projections, both 2023 and 2024 will see record deliveries of close to 2.40 Mteu. Depending on tonnage demand, many of the further-out delivery slots can likely be moved around by a few months.

Incentivized by strong demand, a number of yards have accelerated ship deliveries wherever possible. In many cases, this allowed the builders to negotiate premiums with owners who may benefit from an early delivery. At the same time, accelerating the pipeline allowed yards to market additional newbuilding slots that opened up.

For a fleet size of 25 Mteu, and assuming a realistic usable service life of 25 years for a container vessel, this year’s projected 1.10 Mteu newbuilding tally is essentially a zero-growth replenishment rate.

In other words: Newbuilding deliveries will only slightly alleviate the pain caused by supply chain problems such as port congestion and equipment shortage. However, there will not be a sufficient number of new ships to compensate for the capacity shortfalls caused by the system inefficiencies which are currently swallowing up about one tenth of the ’dynamic’ liner shipping capacity

SITC further improves China - Japan - Vietnam network

SITC (Shandong International Transportation Corporation) will as of next week expand one of its Shanghai-Japan services, the 'SKT6' to include South China and Northern Vietnam. This will further enhance the already comprehensive coverage of the Chinese regional carrier connecting the three countries.

The extended ‘SKT6’ will follow a butterfly pattern which centers at Shanghai. It will continue to serve Nagoya, Yokkaichi, Tokyo and Sendai on one loop and covers Hong Kong, Qinzhou and Haiphong on the other.

SITC will deploy two additional ships, the 907 teu SITC HONG KONG and the 915 teu RESURGENCE, in addition to the 915 teu REFLECTION, which allows the carrier to operate the revised service on a weekly basis.

The first sailing for the expanded ‘SKT6’ is scheduled on 3 March from Shanghai with the RESURGENCE.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

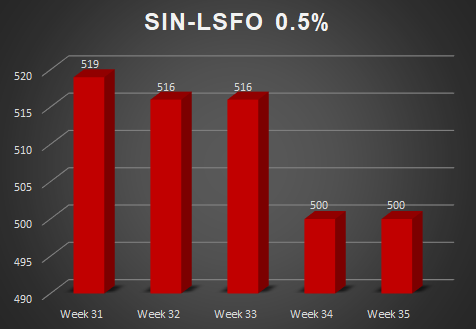

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025