Maritime Market News

News Highlights week: 12 - 2022

Ngày đăng: 24/03/2022 | Lượt xem: 635

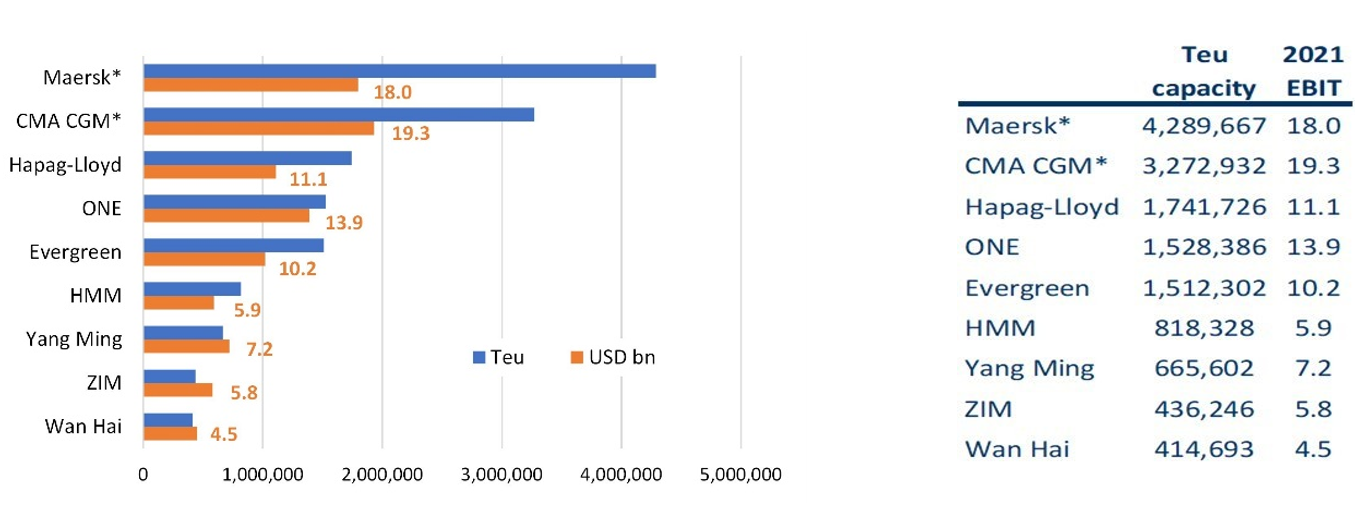

The shipping bonanza continues: Earnings for nine of the topten carriers have already reached USD 95 bn for 2021.

Nine of the ten leading container carriers publishing public numbers have already generated an operating profit (EBIT) of USD 95 bn for 2021, with only COSCO left to report.

Including estimates for COSCO, the ten carriers reported an aggregate operating margin of 57.1% for the final quarter of the year, once again a record for the leading lines.

However, growth slowed sharply in the fourth quarter, suggesting Omicron was not a game-changer for the industry and the extraordinary expansion seen in the middle of last year was not sustained. Carrier liftings and revenue were also limited in growth by the ongoing port congestion which forced them to skip voyages.

Final earnings for the year for the full 10 carriers are expected to be around USD 115 bn, in line with forecasts made by Alphaliner at the end of November when the Omicron variant was first confirmed.

Privately-held MSC which does not publicly release financials is not included in the survey. COSCO will announce its full-year result by March 31 in a break from the usual schedule of carrier reporting where typically CMA CGM has been the last line to publish its results.

Once again, smaller Asian carriers without significant non-shipping activities posted the best operating margins. Taiwan’s Yang Ming closed out 2021 with the highest margin, at 67.8% for the quarter, and the highest overall total for the year, at 61.3%.

With the exception of Q2 when ZIM briefly made an appearance, the four highest ranking companies in 2021 have consistently toggled between Yang Ming, Evergreen, Wan Hai and HMM.

However, Evergreen reported a drop in its operating margin in the final quarter of the year, bucking the industry trend, after company EBIT came in at USD 3.36 bn.

This was flat on Q3 despite higher revenues. The main Taiwanese line still recorded the second highest average margin for the year.

Despite efforts by the four largest carriers to deploy more capacity on the transpacific and the full impact of spot earnings for those carriers with a delayed reporting system, the rankings of Maersk, CMA CGM, COSCO and Hapag-Lloyd remained stable throughout the year, with the lines consistently occupying the bottom four places.

For the 9 carriers which have confirmed their results for this latest year, 2021 EBIT represents a 630% increase over their equivalent figures in 2020.

Overall, the top 10 lines posted operating profits (core Earnings before Interest and Tax) of approximately USD 17 bn in 2020, once estimated earnings for ONE were included. (The Japanese liner grouping did not begin officially reporting EBIT figures until Q1 2021.)

In terms of operating margin, the Q4 2021 average of 57.1% compares to 24.5% for the fourth quarter of 2020, and 2.4% in fourth quarter 2019.

Charter market undeterred by Ukraine war

The container charter market remains so far mostly unaffected by the war in Ukraine.

Only smaller vessels, which account for the bulk of ships plying services to Russia are feeling the effect of the conflict, with many service closures leading to tonnage re-deployment.

Alphaliner has also heard stories of feeder vessel fixtures failing on charterers' subjects, but the phenomenon remains so far limited.

The continued strong demand is anyway helping carriers to easily use ships on other routes, while several charterers remain on the lookout for smaller tonnage in many areas.

Otherwise, the market fundamentals remain unchanged. Demand is staying strong across the board while the availability of tonnage is extremely tight, especially for prompt units.

Charter rates meanwhile continue to evolve at historic highs, but tend to plateau again, after weeks of continued rise.

The number of fixtures remains globally limited, due to a continued scarcity of ships across most sizes.

However, the negative signals on the cargo and oil front continue to raise the spectre of a market correction going forward.

The Shanghai Containerized Freight Index (SCFI) has now been falling for ten consecutive weeks, and although it remains five times higher than prior to the COVID pandemic, its retreat suggests that the cargo demand bonanza might gradually come to an end.

The price of oil meanwhile remains a major concern for the world economy and for shipping, and although it has come off substantially since the peak of USD 130 a barrel recorded a week into the invasion of Ukraine, it is still at its highest level since 2014.

VNS

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

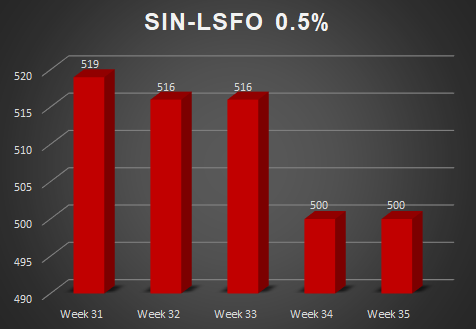

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025