Maritime Market News

News Highlights week: 16 - 2022

Ngày đăng: 22/04/2022 | Lượt xem: 868

OOCL reports record USD 5.1 bn revenue for Q1

Hong Kong based carrier Orient Overseas Container Line (OOCL) has reported unaudited revenue of USD 5.1 bn for the first quarter of the year, beating both the previous two quarters and setting a new record for the carrier.

Compared with the final quarter of 2021, revenues were higher in three of the company’s four trade segments, with only the transatlantic earning less in Q1 than the previous three months - see table below.

Revenue on the transpacific leapt 7% versus October-December despite flat liftings. Revenue also rose by the same amount on the intra -Asia/Australasia trades – OOCL’s biggest segment by volume.

Overall, average rates per teu increased 7% in January-March versus the previous quarter, promising yet more stellar financial results for the carriers.

OOCL’s operational update shows an average USD 2,873 per teu for the COSCO-owned line in the January to March period. This compares to USD 2,673 per teu in the October to December period.

The result was achieved despite severe congestion which crimped liftings. This was most apparent on the transatlantic where volumes dropped 10% compared to the previous quarter.

However, liftings on the transpacific were practically unchanged on the previous three months, dropping less than 1%. Furthermore, perbox earnings on the transpacific reached USD 3,963 per teu in the period.

OOCL reported quarterly revenue of USD 4.9 Bn in Q4 2021 and USD 4.3 bn in Q3 2021

Charter market in ‘wait-and-see’ mode

The container charter market has never been this quiet since Alphaliner started compiling this report, nearly ten years ago. Although the Easter holidays are playing a role in the market’s current lethargy, numerous other factors can explain this situation.

Firstly, supply of prompt tonnage continues to be at an all-time low which is naturally restricting the volume of activity.

Secondly, vessel demand has become less pressing than a few weeks ago, with most charterers adopting a ‘wait-and- see’ approach in response to an ocean of economic and geopolitical uncertainties plaguing the world economy.

Among the headwinds facing shipping lines are the Covid lockdowns in Shanghai with their resulting disruptions on cargo flows, and the ongoing war in Ukraine with its various knock-on effects on seaborne trade.

A slower economic growth in China, and persistent inflationary pressures across the globe undermining consumption are also threats to the current cargo bonanza. It is meanwhile not entirely clear if the continuously falling freight rates on most major routes are ‘only’ a seasonal trend or herald a more serious structural fall in cargo demand, that would reflect a reversal in consumer behavior back to pre-Covid times.

A sharp 35% fall in spot freight rates on the Asia-East Coast of South America trade routes since the beginning the year, partly attributable to a significant drop off in cargo volumes, is certainly food for thought in this respect. Finally, there is the issue of sky-high fuel prices, with little signs that they will ease any time soon considering the current geopolitical tensions with Russia.

Despite these threats, the container charter market is for now showing no sign of weakening. Charter rates remain at historical highs and although there is some softening in the air in certain sizes, there is no significant change of direction expected in the foreseeable future

against a backdrop of continued vessel shortage and supply chain disruption.

VNS

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

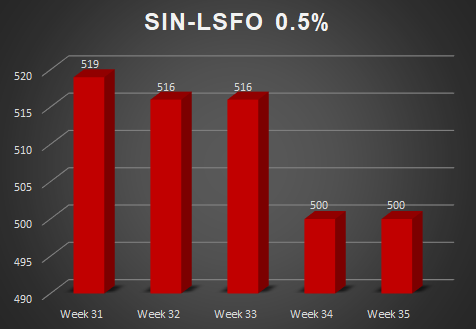

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025