Maritime Market News

News Highlights week: 17 - 2023

Ngày đăng: 28/04/2023 | Lượt xem: 580

Matson predicts 90% drop in shipping income for Q1

US-based Matson Inc has announced preliminary operating income for its Ocean Transportation activities of between USD 23-28 M, representing a drop of more than 90% on the same quarter a year ago.

Lower volumes and freights on the company’s China service were the main driver of the decline: China volumes fell 35.4% year-on-year, a result of the discontinuation of its CCX service in September 2022 and lower demand on its remaining CLX and CLX+ services.

Matson expects improved trade dynamics on the transpacific in the second half of 2023 but promised more year-on-year declines in volumes and rates in the second quarter, as retail companies remain conservative over replenishing inventories.

The contrast with 2022 is stark: Matson logged shipping operating income of USD 416.2 M in Q1 2022, and company net income of USD 339.2 M. Net income is predicted at USD 29-34 M for Q1 2023.

Boxships ordering slows down, but ‘talks’ continue

In spite of an already massive container ship orderbook and far out delivery dates for ships that would be ordered later this year, carriers seem keen on a number of additional newbuilding deals.

For now, activity has slowed down, but industry sources suggest that talks between shipowners and yards continue.

Yang Ming for example, the only major carrier without any new ships in the pipeline, is reportedly making progress with negotiations for a set of 15,000 teu ships to be ordered from a Korean builder.

The Taiwanese carrier already disclosed to the stock exchange that it had launched a procurement process for such tonnage, but it has not placed any actual orders so far.

Originally, Yang Ming invited the yards to provide offers for LNG-dual fuel tonnage, but ship broker reports now suggest that the carrier asked the potential candidates to offer methanol-dual fuel ships instead. The shipping line appears to have reconsidered its ‘green fuel’ options since methanol has recently gained traction as an alternative pathway to cleaner and more sustainable shipping.

Methanol was initially championed by Maersk, but others have joined the methanol train with a fair number of orders for big ships. This includes CMA CGM and COSCO-OOCL.

Methanol is also being considered for a number of deals for small and mid-sized ships in the size range from 2,000 to 4,000 teu that are currently under negotiation. Details of these ‘talks’ however remain scarce for the time being.

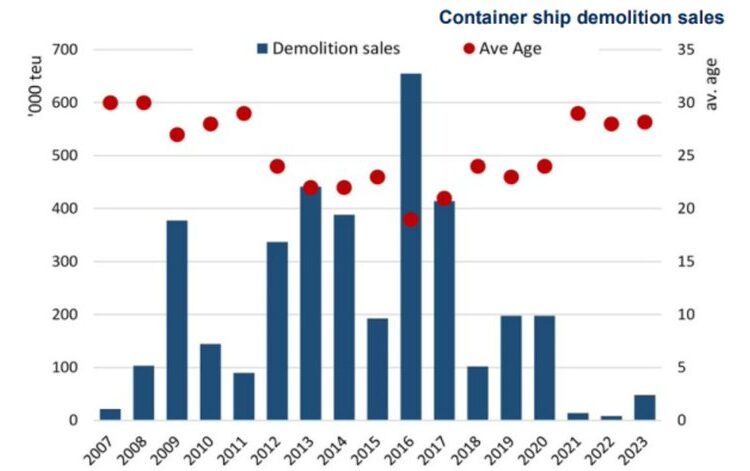

Demolition sales slower than expected in early 2023

Demolition sales have increased at a slower pace than anticipated in the first months of 2023, with only 28 container ships of 500 teu and above for a total of 48,555 teu sold for recycling since 1 January. This is however much higher than last year at the same time, when zero vessels were sold to breakers.

The average age of vessels disposed was at the elevated level of 28 years with most sales concentrated in the 1,000-2,000 teu range at over 80% of transactions by number (23 units). The smallest ship sold for recycling was the 591 teu LEVANT HORIZON and the biggest was the 6,572 teu FLORA. Eighteen of the demolition sales concerned three carriers: Wan Hai disposed of ten of its 1990s-built 1,088-1,368 teu ‘160’ and ‘200’ series ships and the Transworld Group of Singapore sold four 1990s-built 1,600-1,700 units.

Meanwhile, MSC returned to the scrapping scene after a long absence, selling three 1980s-built vessels, the 1,911 teu MSC FLORIANA and 2,098 MSC GIOVANNA, as well as the 4,809 teu MSC VERONIQUE, a former Maersk ship (see page 2). A fourth vessel, the 1,837 teu MSC NORA II, built in 1999 was also sold in the last few days and more sales could follow in the coming months.

While demolition sales to date have now exceeded the total for the previous two years, the pace remains so far below even modest scrap years such as 2019 and 2020. This is mainly the result of an unexpectedly strong charter market, with some owners keen to prolong the commercial life of ships that would have otherwise been torched. However, Alphaliner believes scrapping will continue to gain momentum in the coming months, especially as the massive influx of newbuild tonnage will put rising pressure on tonnage supply, while the CII remains unfavourable for the least efficient, older units.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

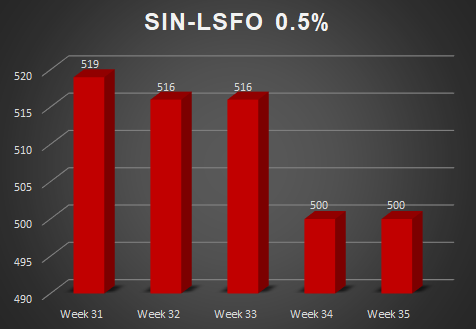

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025