Maritime Market News

News Highlights week: 22 - 2022

Ngày đăng: 02/06/2022 | Lượt xem: 1087

RCL joins China United, Emirates Shipping and Global Feeders on Vietnam - Gulf - Western India loop

Thai carrier Regional Container Lines (RCL) has announced that it will introduce a weekly service between Southeast Asia, the Middle East and the Indian West coast in early June. RCL will market the new offer as its ‘RGA’ loop.

To provide this new service, RCL will become a partner and vessel provider on the loop offered on this trade lane by China United Lines (CULines), Emirates Shipping Lines (ESL) and Global Feeder Shipping (GFS). The three carriers had launched this joint service in January under their respective ‘VGX’, ‘VGI’ and ‘SGS’ respectively.

RCL will begin to participate in the operation as of 6 June and the carrier plans to phase-in its 2,588 teu vessel VIRA BHUM.

This vessel will run alongside the 2,452 teu HUNSA BHUM, another RCL-owned ship that will however operate under charter to CULines.

Emirates Shipping will contribute the the 2,554 teu APOLLON D and Global Feeder Shipping will deploy the 1,841 teu WINNER.

The ‘VGX’ / ‘VGI’ / ‘SGS’ / ‘RGA’ service turns in five weeks and it connects Ho Chi Minh City, Laem Chabang, Port Kelang, Jebel Ali, Sohar, Nhava Sheva, Port Kelang, Ho Chi Minh City.

In addition to providing RCL with a direct link between Vietnam, Thailand, the Middle East and Western India, the loop also features a call at the hub of Port Kelang (Westports). which offers for transhipment options to and from many Far East destinations. This complements RCL already decent coverage between the Far East, Middle East and the Indian West Coast.

Global container vessel order book at record high

Today's container vessel orderbook stands at just under 900 ships and at 6.80 Mteu in terms of overall slot capacity. As such, it is the largest in liner shipping history.

At 6.80 Mteu, the pipeline of new- buildings is bigger than.

> #4 / COSCO Group – 2,92 Mteu

> #5 / Hapag-Lloyd – 1,74 Mteu

> #6 / Evergreen – 1,54 Mteu

...the existing fleets of COSCO, Hapag-Lloyd and Evergreen com- bined.

After a period of ‘neglect' the mid- sized container ship sector has re- gained a reasonable share of the orderbook.

Vessels in the 5,100 to 9,999 teu bracket now account for 16% of all capacity on order. Two years ago, this sector basically did not exist in the nedwbuilding pipeline.

Large NOOs consolidate their power

The 15 leading non-operating owners (NOOs) have increased their share of the market to over 50%, with expan- sion particularly notable among the biggest companies.

Overall, the leading fifteen companies now control 52.7% of the non- operated owned fleet by capacity, versus 48.5% six months ago, and 45.4% eighteen months earlier.

In the six months since Alphaliner’s last survey, Eastern Pacific has risen from 11th to 6th ranking, boosted by deliveries from its pre-pandemic or- derbook. Global Ship Lease rose two places to number 8, while Danaos overtook Zodiac Maritime to become the fourth largest NOO. Both compa- nies were active on the S&P market in 2021.

At the other end of the scale, Mins- heng and SFL Corp fell three places respectively to number 10 and 11 re- spectively, while the Schulte group dropped out of the top 15. It was re- placed by Doun Kisen.

Apart from Eastern Pacific, Japan's Shoei Kisen was the only other NOO to benefit from a significant injection of new orders placed before COVID.

The three leading operators, whose ranking did not change, nevertheless added mass, and Seaspan, Shoei Kisen and Costamare now control 9.8%, 6.2% and 4.7% of the NOO fleet respectively, up from six months ago.

Seaspan, Shoei Kisen, Zodiac, and Eastern Pacific move forward with sizeable orderbooks which will further increase their dominance. Greece's Capital Ship Management is also like- ly to rise up the rankings in future given its 16-ship orderbook.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 05 - Sep | 29 - Aug | CHG | |

| $-VND | 26,510 | 26,502 |  8 8 |

| $-EURO | 0.855 | 0.856 | 1 |

| CNY-VND | 3,754 | 3,754 | 0 |

| SCFI | 1,444 | 1,445 | 1 |

| BUNKER PRICES | ||||

| 05 - Sep | 29 - Aug | CHG | ||

| RTM | 380cst | 391 | 411 | 20 |

| LSFO 0.50% | 452 | 465 | 13 |

|

| MGO | 658 | 650 | 8 |

|

|

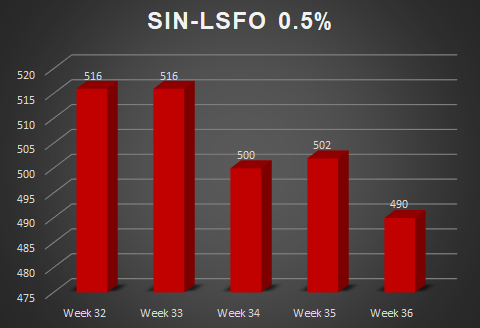

SGP |

380cst | 405 | 412 | 7 |

| LSFO 0.50% | 490 | 502 | 12 |

|

| MGO | 670 | 648 | 22 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025