Maritime Market News

News Highlights week: 24 - 2022

Ngày đăng: 16/06/2022 | Lượt xem: 576

South Korean carriers team up in China-Korea-Vietnam -Thailand trade

South Korean operators HMM, Pan Ocean and SM Lines will in late June launch a weekly service between South Korea, China, Southern Vietnam and Thailand.

This upcoming service, marketed as ‘CVT’, will turn in three weeks calling Incheon, Qingdao, Shanghai, Ho Chi Minh City (SP-ITC), Laem Chabang, Chiwan, Incheon. HMM will deploy the 1,809 teu SKY RAINBOW, Pan Ocean will operate the 1,809 teu POS HOCHIMINH, and SM Line will add the 1,708 teu JAN.

The maiden voyage of the ‘CVT’ is scheduled to start on 26 June from Incheon with the SKY RAINBOW. For all three South Korean carriers, the new ‘CVT’ will further enhance their already decent coverage between these four countries.

MSC upgrades Far East – USEC ‘Santana service’

Three 8,200 – 8,760 teu ships have joined the MSC standalone North Vietnam – Central China – US East Coast ‘Santana’ service in the past weeks as replacement for smaller 4,400 – 5,100 teu classic panamax ships. These include the 4,943 teu MSC DAISY and 5,086 teu MSC CORNELIA, which are currently on USEC – North Europe voyages.

The capacity upgrade will be continued in the upcoming weeks as the 8,100 – 9,640 teu CONTI CHIVALRY, MSC ELMA, MSC ABY, MSC TIANSHAN and MSC CHARLESTON are also lined up to join this Asia – USEC loop.

The ‘Santana’ service was initially launched in August 2020 as a MSC standalone Far East – USWC service. This Transpacific loop was closed in November 2021 and part of the fleet was transferred to a new Far East – USEC service retaining ‘Santana’ as brand name.

The new ‘Santana’ started turning in ten weeks serving Haiphong, Shanghai, Ningbo, Charleston, New York, Haiphong, but meanwhile also serves Houston and occasionally other ports on an ad hoc basis such as Busan or Cristobal.

Charter market holds firm, but clouds building on the horizon

The container charter market remains extremely quiet, with the number of fixtures (only fifteen over two weeks) at an historic low. Both the shortage of ships, especially prompt units, and a cooling of demand explain this situation.

In spite of this rock-bottom activity, the few fixtures agreed are concluded at continuously strong rates, which has led Alphaliner to revise upwards some of its charter rate estimates.

However, the overall market sentiment remains mixed. On the one hand, persistent congestion issues in various ports around the world and the approach of the peak cargo season are expected to underpin demand and keep charter rates at very high levels in the short term, against a backdrop of continued shortage of ships.

On the other hand, clouds continue to build up on a macro- economic and geopolitical level. Inflation is increasingly taking its toll on consumers with continuously rising food and energy prices, while the amount of spending on travels and services is rising at the expenses of goods.

The economic growth in many Western Nations remains meanwhile low, with a risk of recession in some areas impacting consumers’ confidence. These factors are increasingly affecting cargo volumes, with the industry growingly concerned about the evolution of demand in the coming months.

Although the SCFI is now registering its fourth week of (modest) increase, most East-West routes continue to see receding spot cargo rates. Globally, volumes are down compared to a year ago and are only marginally above their 2019 level, prior to the Covid pandemic.

The geopolitical tensions surrounding the conflict in Ukraine and the continuous war of words between the US and China over the Taiwan question are meanwhile doing nothing to boost consumers’ confidence.

While these uncertainties seem to be manageable for containership owners and shipping lines in the short term, the avalanche of newbuilding tonnage expected to hit the market in 2023 and 2024 could see the return of overcapacity and low rates, especially if cargo volumes continue to falter.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

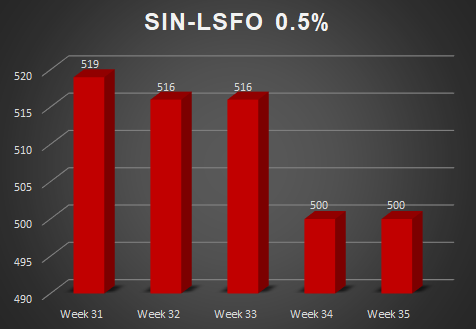

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025