Maritime Market News

News Highlights week: 24 - 2023

Ngày đăng: 15/06/2023 | Lượt xem: 686

ASL reorganizes China – Vietnam coverage

Asean Seas Line (ASL) reorganized its China – Vietnam coverage earlier this month. The Hong Kong-based regional carrier expanded its Central China – Philippines ‘NPX2’ service to South China and Northern / Central Vietnam. This updated ‘NPX2’ will cover ASL’s South China - Northern / Central Vietnam ‘BDX’ service.

The ‘BDX’, which was initially launched in December 2021, is closing this month with a last sailing of the 848 teu PACIFIC GRACE from Nansha on 5 June. This loop used to provide ASL with a weekly connection between Hong Kong, Shekou and Nansha, with Haiphong and Da Nang.

In accommodating the additional calls at Nansha, Shekou, Haiphong, Da Nang and Hong Kong, the revised ‘NPX2’ has extended its turnaround time from two to three weeks.

The updated ‘NPX2’ now operates three 600 -1,100 teu ships serving Qingdao, Shanghai, Manila (S), Nansha, Shekou, Haiphong, Da Nang, Nansha, Hong Kong, Qingdao. The 1,078 teu DANUM 168 was the first ship that followed the expanded rotation of the ‘NPX2’ with its departure from Qingdao on 5 June.

At the same time, ASL is ending its standalone South China – Southern Vietnam ‘BHX’ loop. This South China - Southern Vietnam segment will be covered by the recently improved South China-VietnamPhilippines ‘SVP’ service, offered in partnership with Emirates Shipping Lines (ESL) and Pacific International Lines (PIL) (see NL 2023 - 22). Besides extending the 'SVP' to South China at the expense of Cebu in the Philippines, ASL is also upgrading from a slot operator to a vessel provider.

Charter market not on holiday yet!

The container charter market appeared at first glance a little quieter in the past two weeks giving the impression that an (early) summer lull was already taking its toll on the activity. However, there has been a lot happening behind closed doors with multiple deals concluded in the larger sizes including for newbuildings. This high activity is obviously supporting charter rates which remain very healthy for big ships, particularly for long periods.

By contrast demand for smaller tonnage seems to be running out of steam, with charter rates showing a slight contraction in the 2,000- 2,699 teu and 1,000-1,249 teu sizes, particularly for older standard tonnage.

Across the board there is increasingly a two-tier market with on the one hand, much sought-after modern, energy efficient, ‘CII-friendly’ tonnage that gets fixed at continuously strong rates and, on the other hand, older, less energy-efficient ships that have to accept less favourable terms. This trend will become more and more marked in the coming years, ultimately forcing the retirement of the least efficient ships, especially as overcapacity makes its comeback.

On the cargo front, the news is mixed. Signs that volumes have been picking up on a number of key routes in the past weeks is bringing back optimism among carriers. The peak cargo season could therefore be slightly better than expected, which would obviously help absorb the continued influx of newbuilding tonnage. On the other hand, cargo freight rates remain far too low, forcing shipping lines to run at a loss on many routes. Labor issues on the US West Coast and draft restrictions at the Panama Canal have been pushing rates up a bit, but this is clearly only a temporary fix. The fact is that too much newbuilding capacity continues to plague the market and contributes to keeping cargo rates at unsatisfactory levels. A lot moreslow steaming and ship scrapping is therefore needed to see the market durably recover.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

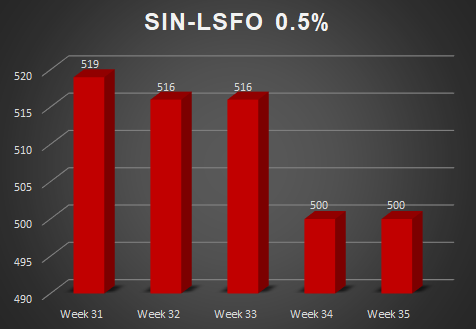

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025