Maritime Market News

News Highlights week: 26 - 2023

Ngày đăng: 29/06/2023 | Lượt xem: 828

Wan Hai and IAL revise Japan – Southeast Asia ‘NS5’

Wan Hai Lines (WHL) and Interasia Lines (IAL) will in early July revise their joint ‘New Super 5’ (‘NS5’) service that covers Japan, Taiwan, South China, Vietnam and Malaysia.

The modified ‘NS5’ will thereafter add weekly calls at Taipei. These will come at the expense of Keelung and Hong Kong on the southbound segment of the loop.

As from the departure of the 2,038 teu WAN HAI 295 from Tokyo on 4 July, the updated ‘NS5’ will continue to turn in four weeks with four 1,600 – 2,000 teu ships.

It will serve Tokyo, Yokohama, Kawasaki, Taipei, Taichung, Ho Chi Minh City (Cat Lai), Port Kelang (Northport), Penang, Ho Chi Minh City (Cat Lai), Hong Kong, Shekou, Tokyo.

ONE, PIL, TS Lines and Namsung launch Korea - China - Straits - Vietnam service

Ocean Network Express (ONE), Pacific International Lines (PIL), TS Lines and Namsung Shipping will early next month launch a South Korea - China - Straits - Southern Vietnam service which will be marketed as ‘KCS2’, ‘KCS’, ‘KMV2’ and ‘NFS’ by the respective carriers.

The upcoming ‘KCS2/KCS/KMV2/NFS’ service will turn in four weeks with four 2,000 – 2,900 teu ships.

It will call at Busan, Kwangyang, Shanghai, Chiwan, Singapore, Port Kelang (Westport), Penang, Singapore, Ho Chi Minh City (Cat Lai), Nansha, Busan.

The four partners are set to deploy the 2,034 teu KOTA JOHAN, the 2,433 teu SITC MINGCHENG, the soon-to-be delivered 2,900 teu TS VANCOUVER, and the 2,553 teu LOS ANDES BRIDGE.

The latter is scheduled to begin the loop’s maiden voyage when it sails from Busan on 6 July.

Besides enhancing overall China - Korea - Straits - Vietnam coverage of the four partners, the upcoming loop will also provide a direct connection between South Korea and Penang in Malaysia.

Charter market: rates soften in the smaller sizes

Activity in the container charter market has slowed down in the past days, ending a busy period of fixing, particularly in the larger sizes.

However, big ships are still in demand and Alphaliner has registered further fixtures of compact newbuildings of 7,000 and 5,900 teu chartered for multi-year employments at continuously healthy rate levels.

More charter deals would likely be concluded if a greater number of vessels was available, especially prompt units, but the market remains sold out in the larger sizes. In the mid-size range, ‘classic panamaxes’ of 4,000-5,299 teu and units of 3,000-3,800 teu are still in demand, but the shortage of ships is limiting the activity and supports strong charter rate levels.

Below 3,000 teu, the market has a different flavor. Supply is on the rise, particularly (but not only) in the 1,700-1,900 teu segment where a substantial build-up of tonnage and the return of ‘spot’ vessels is beginning to take its toll on charter rates. Alphaliner is already observing reduced rates and shorter periods for those unemployed vessels sitting idle, and unless demand picks up strongly in the coming weeks, this trend could also hit vessels with a more forward position, especially in Asia.

Globally the market outlook remains highly uncertain for nonoperating owners (NOO) due to a continuously grim macro-economic environment. On the cargo side, the peak season is bound to be subdued in spite of positive signs on volumes here and there and the strong performance of some trade routes such as Asia-Med or Asia-South America. On the supply front, the continued influx of newbuildings is meanwhile significantly contributing to keeping cargo rates at depressed levels, forcing carriers to operate a number of services at a loss.

More capacity thus needs to be withdrawn from the market, but this is not really happening, with demolition sales remaining at disappointing levels. Only slow steaming is for now, in part, the growing overcapacity issues but this has so far been insufficient to prompt a sustainable recovery in cargo freight rates.

As a result, Alphaliner remains cautious about the sustainability of the current strong charter market and expects more weakness further down the road.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 05 - Sep | 29 - Aug | CHG | |

| $-VND | 26,510 | 26,502 |  8 8 |

| $-EURO | 0.855 | 0.856 | 1 |

| CNY-VND | 3,754 | 3,754 | 0 |

| SCFI | 1,444 | 1,445 | 1 |

| BUNKER PRICES | ||||

| 05 - Sep | 29 - Aug | CHG | ||

| RTM | 380cst | 391 | 411 | 20 |

| LSFO 0.50% | 452 | 465 | 13 |

|

| MGO | 658 | 650 | 8 |

|

|

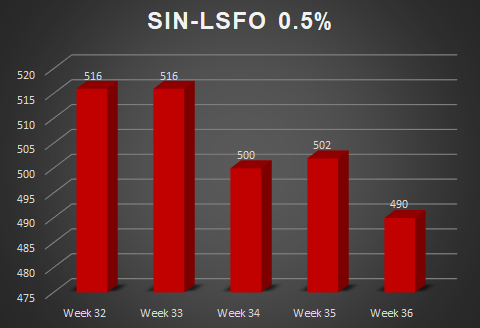

SGP |

380cst | 405 | 412 | 7 |

| LSFO 0.50% | 490 | 502 | 12 |

|

| MGO | 670 | 648 | 22 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025