Maritime Market News

News Highlights week: 36-2021

Ngày đăng: 09/09/2021 | Lượt xem: 643

OOIL reports USD 2.9 bn operating profit in H1

OOCL parent company OOIL has reported a net profit of USD 2.9 bn for the first half of 2021, versus a gain of just USD 102 M in the equivalent period in 2020.

Revenue more than doubled to USD 6.9 bn, from USD 3.4 bn in H1 2020. The COSCO subsidiary, which publishes financials every half year, said EBIT from its container transport and logistics operations came in at USD 2.8 bn in the six-month period, equivalent to a 40.9% operating margin. Liftings for OOCL rose 19% compared to H1 2020, while loadable capacity increased 14%.

OOCL recently ordered ten 16,000 teu newbuildings at Chinese shipyards NACKS and DACKS at a cost of approximately USD 157.5 M per ship. It will start to take delivery of the first of twelve 23,000 teu vessels ordered last year from 2023 onwards.

Operating margins exceed 50% for several carriers in Q2

Container carriers’ average operating margin rose to a record 44.4% in Q2 2021, versus 38.2% in the previous quarter, as lines’ business output was boosted by another jump in rates.

As expected, all ten lines increased their margins compared to the first quarter, with results for medium sized Asian operators Yang Ming, Evergreen and HMM, which led the pack, exceeding 50% for the first time (58.4%, 53.2% and 50.5% respectively). Maersk group reported the lowest margin at 28.7%.

Weak container volume growth, which averaged just 4% quarter-on-quarter, was offset by the large increase in rates. The average dollar amount per teu of the ten lines surveyed rose 15% compared to the previous quarter. The slight increase in bunker prices in the quarter had little impact.

Charter market continues to flourish

Despite a low level of activity essentially due to a lack of tonnage, the charter market is still flourishing, as demand continues to far outstrip supply.

The market is still very much two-tier, with short employment being negotiated at stratospheric figures, up to USD 200,000 per day for some ships, while the more conventional 24 month and 36 month charters are commanding significantly lower, albeit historically high, rates.

However, while a number of fixtures continue to be agreed at ever stronger rates, there is a trend towards some price stabilization, especially in the classic panamax 2,800-3,800 teu sizes as well as between 1,500-1,900 teu, where rates seem to be plateauing.

Whether this signals that the peak is gradually being reached is up for discussion. Meanwhile, the continued short supply of tonnage bodes well for NOOs in the short and medium term in the face of an ongoing robust demand from carriers, fuelled by continuously sky-high freight rates and cargo volumes.

Even the forthcoming Golden Week in China in early October, a traditionally slower period for the world container trade, is unlikely to put a break on the demand for tonnage, with signs that liner shipping companies will blank fewer sailings than in previous years.

Carriers should therefore not expect any weakening in the charter market any time soon, and are left with the choice of pricey and longterm charter commitments, or alternatively the purchase of tonnage.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 05 - Sep | 29 - Aug | CHG | |

| $-VND | 26,510 | 26,502 |  8 8 |

| $-EURO | 0.855 | 0.856 | 1 |

| CNY-VND | 3,754 | 3,754 | 0 |

| SCFI | 1,444 | 1,445 | 1 |

| BUNKER PRICES | ||||

| 05 - Sep | 29 - Aug | CHG | ||

| RTM | 380cst | 391 | 411 | 20 |

| LSFO 0.50% | 452 | 465 | 13 |

|

| MGO | 658 | 650 | 8 |

|

|

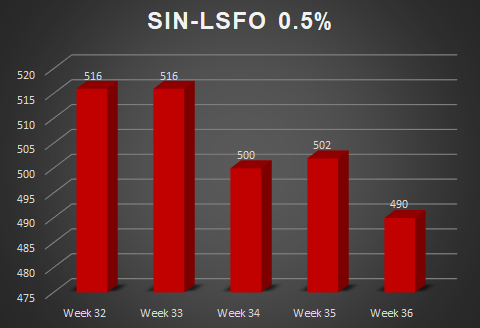

SGP |

380cst | 405 | 412 | 7 |

| LSFO 0.50% | 490 | 502 | 12 |

|

| MGO | 670 | 648 | 22 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025