Maritime Market News

News Highlights week: 37 - 2023

Ngày đăng: 15/09/2023 | Lượt xem: 530

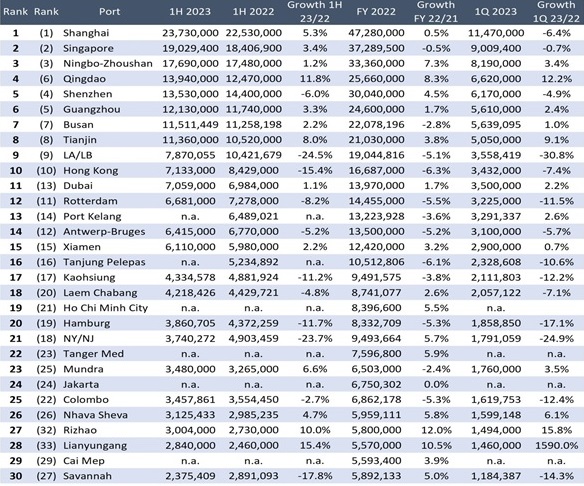

Port throughput drops sharply in Europe and the US

The six European and American ports featuring in the Top 30 ranking of major container ports showed across-the-board declines in throughput in the first half of the year, as the impact of economic contraction in the west took effect.

Los Angeles/Long Beach, New York/New Jersey, Savannah, Rotterdam, Antwerp-Bruges and Hamburg reported volume reductions of between 5% and 25% in January-June. At the lower end, Antwerp-Bruge’s 5% drop was artificially boosted by its merger with Zeebrugge in 2022 and would otherwise have been even more severe, while the three US ports recorded the biggest declines, a clear reflection of the economic downturn since the pandemic.

Los Angeles/Long Beach saw a net loss of 2.6 Mteu in traffic versus the same period in 2022, or a 25% fall in volumes. It remains to be seen if the recent signing of a new labour agreement for west coast dockworkers can help the port claw back some of the business lost to east coast ports over the past two years in what is clearly a difficult economic environment. US east coast ports also logged severe declines, with New York/New Jersey reporting a 24% drop in traffic versus a year ago, and Savannah an 18% decline.

China reports very strong first half of the year. Despite recent export softness, China reported a very strong half year: total volumes processed across the country’s ports reached 149.2 Mteu, a rise of 4.8%. Shanghai posted an impressive 5.3% year-on-year increase despite a poor performance in the first quarter following congestion and COVID-related issues.

Chinese throughput may not hold up, however, with export data showing rapidly declining figures. The country reported its lowest export figures in more than three years in July, although the decline slowed in August.

Mid-size Asian ports did not perform as well: Kaohsiung and Laem Chabang both reported a drop in traffic in H1, at a rate of –11.2% and –4.8% respectively.

By contrast, Port Klang, which has yet to report half-year figures, predicted it would increase volumes by just over 2% over the full year to 13.5 Mteu, regaining some of the 500,000 teu lost in 2022.

Mundra and Dubai rise in the rankings. In the Middle East/Indian sub continent, both India’s major ports recorded traffic increases, but Mundra eased further ahead of Nhava Sheva, handling 355,000 teu more than its rival, and consolidating its lead since surpassing its competitor in 2020.

Dubai overtook Rotterdam in the rankings on the back of a modest 1.1% increase in throughput to 7.1 Mteu. Rotterdam volumes fell more than 8% in the same period.

The Middle East port could potentially overtake Hong Kong in the rankings in future, as the latter appears on course to drop out of the top 10 for the first time either this year or next following six consecutive years of volume declines.

Hapag-Lloyd blanks twelve Asia-Europe sailings

Following the example of MSC and Maersk, Hapag-Lloyd has also announced capacity adjustments to its network.

The German carrier cites forecasted reductions in demand as reasons for the cuts, especially the upcoming Golden Week Holidays in China, which will fall into the first week of October.

Twelve sailings from Far East are cancelled in weeks 39 to 43, seven of which to North Europe and the five to the Mediterranean.

Most of these sailings concern voyages of THE Alliance, but Hapag Lloyd also confirmed a voided sailing in week 39 from Qingdao on its ‘FE9’ loop. Hapag-Lloyd offers this connection through a slot charter on the OCEAN Alliance’s fifth Asia – North Europe loop, operated by CMA CGM as ‘FAL3’.

Spot ocean freight rates from Shanghai to North Europe took another 7% hit last week, according to the Shanghai Containerized Freight Index (SCFI). Rates were down to USD 1,428/feu. Shanghai to West Med rates maintained a notably higher level at USD 2,612/feu, but were also down 4.1% week-on-week.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

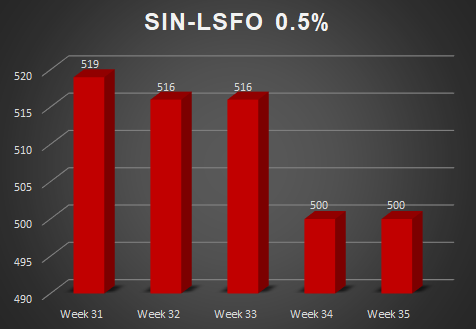

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025