Maritime Market News

News Highlights week: 42 - 2022

Ngày đăng: 20/10/2022 | Lượt xem: 495

Charter market continues to weaken.

The container charter market remains dull, with a low level of activity, which has however slightly picked up since the end of the Golden Week holiday in China.

All the signals are currently negative for Non-Operating Owners (NOOs): demand is weak, supply continues to rise, charter rates are losing further ground (albeit at a slower pace than seen recently) and the business on offer is mostly for short employments, often combined with options.

Charterers are striving for new lower benchmark rates with every new fixture, but NOOs are trying to resist, arguing that the environment is not that bad, with a continued limited supply of quality prompt tonnage in some size segments.

But the bottom line is the fast deterioration of the cargo environment, which does not bode well for charter rates in the short & medium term, as the weakening volumes are unlikely going to stimulate demand for tonnage any time soon.

Carriers are trying hard to stem this volume contraction and the freight rate collapse by blanking sailings, removing capacity, shutting down or merging services and reducing speed, but this has been so far insufficient to reverse the trend.

Reports of ships sailing at only 70-80% capacity on main trade routes are showing the extent of the problem and point to further unavoidable capacity reductions further down the road.

Easing congestion around the world is not helping, as capacities held up for weeks are now gradually returning to the market.

Alphaliner believes that, based on the current weak fundamentals, geopolitical instability and poor macroeconomics, the market will remain bearish until at least early 2023, with an unprecedented cost of living crisis slowly pushing the world into a global recession.

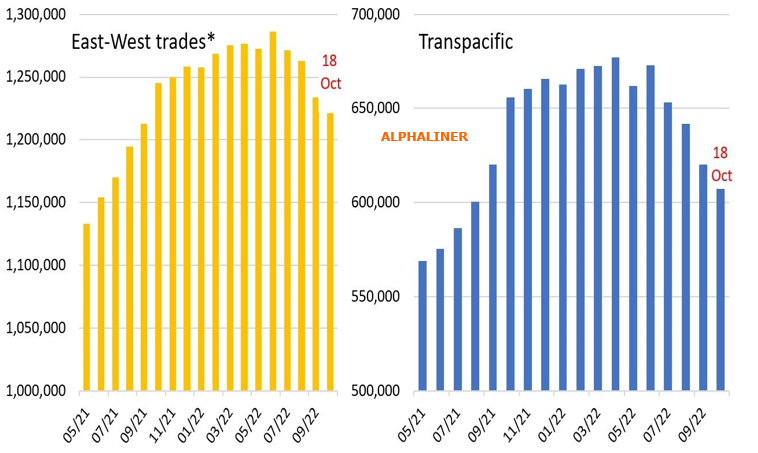

Transpacific capacity falls 10% with no end in sight

This week’s Alphaliner newsletter reports the closure of four more Transpacific loops, while also shedding light on three new Transatlantic initiatives by Kalypso Compagnia di Navigazione (Rifline), CMA CGM, and COSCO Shipping Lines.

Weekly capacity between Europe and North America on 18 October stood at 170,500 teu, up 13.3% since the beginning of the year. The current offering between the Far East and Europe remains fairly stable with almost 442,000 teu of weekly nominal capacity available, compared to 450,750 teu in August. No major Asia – Europe loops have been closed yet, as the 2% capacity reduction is primarily due to the voiding of individual sailings.

Current weekly capacity between Asia and North America however (608,658 teu on 18 October) is already down 10% since its peak in April 2022. This figure will further decrease in the upcoming weeks as more Transpacific loops are closed.

The capacity reductions on the Transpacific are the main reason why overall East West weekly capacity has decreased over the last months.

The shift in carriers’ attention is not only triggered by lower cargo demand for exports ex China, but also by spot ocean freight rate changes. The latest Shanghai Containerized Freight Index (SCFI) figures suggest that Shanghai – Los Angeles/Long Beach rates were down to only USD 2,100/feu as of Friday 14 October, which compares to over USD 15,000 at the beginning of this year.

Meanwhile Shanghai – North Europe rates have fallen from nearly USD 15,600/feu as of 14 January 2022 to a current rate of USD 5,160.

The Shanghai Shipping Exchange of course does not report on Transatlantic rates, but other rate indices estimate current freight rates between Rotterdam and New York to be between USD 7,000 and USD 7,300, which by far exceeds the rates on the two bigger East West trades.

MKT

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

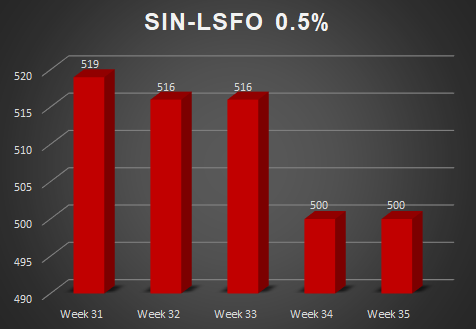

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025