Maritime Market News

News Highlights week: 44 - 2022

Ngày đăng: 04/11/2022 | Lượt xem: 590

The rate of container spot rate decline ticked up again

The rate of container spot rate decline ticked up again this week, with the Shanghai Containerised Freight Index falling another 4.6% to 1,697 points, after dipping just 2% last week. While not as steep as falls in September, which saw four weeks of declines of over 10%, the speed and direction of travel will remain concerning for carriers. The SCFI comprehensive index has now fallen 67% since its peak in January, with rates on some trade lanes now a third of where they were at the top of the market.

Oil will make up just 15% of liquid fuels used to power the shipping fleet by 2050 if the maritime sector is to play its part in limiting man-made temperature rises to 1.5C, according to the International Energy Agency. Shipping would have to undergo a major transformation from heavy reliance on oil to a position in which ammonia meets about 45% of demand for shipping fuel, with bioenergy and hydrogen each hitting a further 20% each, the 31-nation IEA said in its annual forecast. Hydrogen would be focused on short to mid-range operations while electricity will play a minor role on meeting demand from small ships and short distance cruise ferries, according to the IEA’s World Energy Outlook 2022.

Lockdown fallout continues to affect the logistics sector in China’s key shipping hub of Ningbo, though the situation shows some signs of improving. In Beilun district, where several large container terminals are located, lockdowns have been lifted in nine of the 11 subdistricts and part of the other two regions, as new coronavirus cases wane, according to the latest government update. A total of 31 storage yards and warehouses have been reopened, compared with 17 in the middle of last week.

Charter market: signs that it might be bottoming out

After weeks of dull activity, essentially caused by a subdued demand, the charter market has ‘woken up’ in the past fortnight.

It has experienced a significant rise in the number of fixtures concluded and seen the return of the large mainstream carriers such as CMA CGM, which has been busy fixing or extending a dozen vessels.

Ships of 1,700-1,800 teu and 1,000-1,250 teu have been in particularly high demand with about twelve fixtures agreed in each segment.

This rally has helped reduce the fleet of spot ships in these sizes from a total of ten units to only three.

However, charter rates in both sizes have continued to lose ground, with standard 1,700 teu tonnage now fixing at only USD 14,000 per day and units of 1,000 teu obtaining around USD 11-12,000.

These figures are four times lower than what NOOs could achieve at the peak of the market in March.

The rest of the market is also seeing continuously weakening charter rates, like for example ‘classic panamaxes’ (4,000-5,299 teu) which are now getting fixed at low-USD 20,000s for periods of six months, a new significant downward correction.

This negative trend on the charter rates could however come to an end soon, considering the reduction in the number of spot ships and the continued limited prompt supply of tonnage in most sizes.

But hoping for a rate rebound is probably premature, in view of the continuously grim envsuent on the cargo side.

On Friday, the Shanghai Container Freight Index (SCFI) which reviews spot cargo rates reached a new low at 1,697 points, down 4.6% from the previous week.

The SCFI is now nearly four times below its January 2022 peak but is still about twice as high as before Covid.

The question is to know how low cargo rates will fall, with attempts by carriers to stem the decline through service closures, blank sailings and reduced speed having so far proven insufficient.

More capacity needs to be structurally removed from the market to fix the overcapacity issue and demolition is obviously the most obvious option coming to mind.

But en masse scrapping might not happen just yet, with both cargo and charter rates probably not low enough, for now, to prompt NOOs and carriers to start getting rid of their older tonnage.

MKT

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

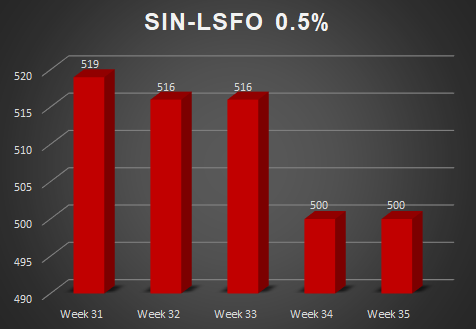

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025