Maritime Market News

News Highlights week: 44 - 2024

Ngày đăng: 31/10/2024 | Lượt xem: 569

COSCO buys into Laem Chabang container terminals

COSCO SHIPPING Ports Limited (CSPL) on 23 October announced that it acquired 12.5% and 30.0% of the equity stakes in Thai Laemchabang Terminal Company (TLT) and Hutchison Laemchabang Terminal (HLT), respectively.

The Chinese firm agreed to pay approximately USD 110 M for the two stakes. With the buy-in, COSCO Group becomes a minority shareholder in several container terminals (or terminal modules) at the Thai main port of Laem Chabang, which is located some 100 km south of central Bangkok.

COSCO will henceforth have stakes in the terminals modules A2 through TLT, as well as modules A3, C1-C2 and D1-D3 through HLT.

While the Port of Bangkok, where vessel size remains limited to the well-known ‘Bangkokmax’ (1,900 teu) and ‘Max-Bangkokmax’ (2,300 teu) ships, remains very popular, Laem Chabang is basically the main container port for the greater Bangkok region and all of Thailand. It accounts for some 80% of total throughput in the country.

CSPL commented that the acquisition would ’help further develop the trade and economic ties between China and Thailand’. The company added that it would also ’help COSCO SHIPPING Ports optimize the layout of port resources and deepen the synergies between port and shipping companies’.

On a global scale, Laem Chabang ranks 17th with an annual throughput of 8.87 Mteu in 2023. Currently, there are ten separate concessions operating container piers at Laem Chabang. These reach from small facilities, designed for barges and feeders, to large mainline terminals that can handle ‘megamax’ ships.

No weakness in sight for charter market

The container charter market continues to do very well for tonnage providers with demand showing no sign of easing, whilst a continued limited supply of ships is supporting healthy charter rates.

Most size segments enjoy the bonanza but the larger sizes above 4,000 teu are the ones which benefit the most from the current situation as the persistent low availability of prompt tonnage is forcing charterers to pay continuously strong monies to obtain the ships they want. Forward fixing well into 2025 continues to be the name of the game although Alphaliner hears that some carriers are becoming a little reluctant to fix vintage tonnage well in advance, giving instead their clear preference to modern and eco units.

In the smaller sizes under 4,000 teu, the last couple of weeks have seen a healthy volume of fixing with the number of fixtures concluded substantially higher than in previous weeks. The 2,000-2,600 teu, 1,500-1,900 teu, 1,000-1,249 teu and sub-1,000 teu sizes were particularly busy. However, and contrary to developments in the large sizes, charter rates are not making any significant progress due, in part, to a greater availability of tonnage.

Nevertheless, the charter market’s continued good health is astonishing considering the various headwinds the sector is facing. Firstly, the peak freight season is behind us, so cargo volumes would be expected to be lower at this time of the year. Secondly, newbuildings continue to flood the market and would under ‘normal’ circumstances start taking their toll on the market. But this is not happening, as the Cape of Good Hope diversions continue to support demand, while cargo volumes are higher than initially expected on many routes.

On Friday, the Shanghai Containerized Freight Index (SCFI) reflected this ‘bullishness’, and was up by a strong 6%, ending fourteen weeks of consecutive fall. Whether the GRIs implemented by carriers will stick through November remains to be seen but for now, and despite negative external factors, particularly new ship deliveries, the market is holding much better than anybody was initially predicting.

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 03 - Oct | 26 - Sep | CHG | |

| $-VND | 26,420 | 26,453 |  33 33 |

| $-EURO | 0.852 | 0.855 | 3 |

| CNY-VND | 3,764 | 3,759 | 5 |

| SCFI | 1,115 | 1,115 | 0 |

| BUNKER PRICES | ||||

| 03 - Oct | 26 - Sep | CHG | ||

| RTM | 380cst | 397 | 418 | 21 |

| LSFO 0.50% | 434 | 463 | 29 |

|

| MGO | 659 | 695 | 36 |

|

|

SGP |

380cst | 407 | 424 | 17 |

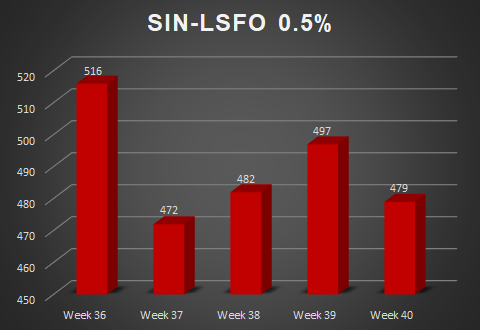

| LSFO 0.50% | 497 | 497 | 0 |

|

| MGO | 679 | 702 | 23 |

|

Tin nổi bật

-

-

Nghị quyết Hội đồng quản trị ngày 01/10/2025

Ngày 02/10/2025

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025