Maritime Market News

News Highlights week: 47 - 2022

Ngày đăng: 26/11/2022 | Lượt xem: 620

Namsung adds Indonesia to South East Asia coverage

South Korean operator Namsung Shipping will next month expand its Southeast Asia coverage to include Indonesia.

The carrier is set to join its compatriot KMTC and Sinokor on their jointly operated ‘ANX’ service, which connects South Korea, Central and South China, Southern Vietnam, Thailand and Indonesia.

Namsung will deploy its newly delivered 1,607 teu PEGASUS PROTO, which is scheduled to join the ‘ANX’ service on 10 December at Incheon. This sailing also marks the start of Namsung's participation on this upcoming loop.

The ‘ANX’ turns in four weeks using four ships of 1,600 – 2,500 teu calling at Inchon, Busan, Ulsan, Shanghai, Ho Chi Minh City (Cat Lai), Laem Chabang, Jakarta, Ho Chi Minh City (Cat Lai), Hong Kong, Chiwan, Inchon.

he upcoming 'ANX' will not only provide a direct access to Indonesia's main port Jakarta, but it will also improve Namsung's current coverage between South Korea, China, Southern Vietnam and Thailand.

Spot ocean rates in China close to pre-pandemic levels

The pressure on Chinese export spot ocean freight rates has increased in the past few weeks. Shanghai – North Europe rates declined 20.7% last week according to the Shanghai Containerized Freight Index (SCFI) after two consecutive weeks with a 16% decline.

The significantly lower spot rates on this route were largely responsible for last week’s overall 9.5% decrease of the index as published last Friday 18 November by the Shanghai Shipping Exchange. The SCFI also showed strong rates declines on the routes from Shanghai to Melbourne (-20.3%), Dubai (-15.6%) and Santos (-12.5%).

The index was down last Friday to 1,307 points which is comparable to September 2020 levels and not so far off from the 1,000 points mark of January 2020. The index has already fallen 74% since its historical high of 5,110 points on 7 Jan 2022.

At the beginning of the year most people in the liner shipping industry expected a slow normalization of the market. It took the SCFI until the second half of July to drop below the 4,000 point mark.

The pace of descent has increased since: it took only another six weeks to fall below 3,000 points (early September) and another four weeks to drop below the 2,000 mark. If spot ocean freight rates remain under the same pressure as in the past few weeks, the index will be back at pre-pandemic levels in December.

Rates from Shanghai to North European base ports reached an alltime high on 14 January (almost USD 15,600/feu), but were down 85% to only USD 2,350/feu last week. Interestingly, Shanghai – West Med spot rates still stand at a higher USD 4,000/feu despite the shorter sailing distance.

Transpacific spot rates fell from a high of USD 8,100/feu in February to only USD 1,550 last week between Shanghai and California (-81%), while the China-US east coast trade saw a rate decrease of some USD 11,800 in January to almost USD 3,900 (-67%).

Of note, actual freight rates paid by shippers in early 2022 were even higher, as the SCFI did not take into account the extra premiums paid for booking guarantees.

Time charterers will take responsibility for a ship’s emissions when the International Maritime Organization’s new Carbon Intensity Indicator, known as CII, is introduced next year.

Under a new clause drawn up by BIMCO’s documentary committee, when entering into the charterparty or incorporating the clause into an existing charterparty, the parties are to agree on a specific CII to be achieved each year, according to a statement.

Imports at Los Angeles and Long Beach continued to decline in October, dropping 28% and 23.7%, respectively, from the year-earlier period. Los Angeles had its worst October for imports in 20 years, while Long Beach’s was its weakest October since 2012. Year-to-date, imports are down 8.6% and 0.1%, respectively, but remain elevated compared to any year prior. Combined, this is the slowest year for the San Pedro Bay ports since 2011.

MKT

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 29 - Aug | 22 - Aug | CHG | |

| $-VND | 26,520 | 26,502 |  18 18 |

| $-EURO | 0.857 | 0.853 | 4 |

| CNY-VND | 3,727 | 3,754 | 27 |

| SCFI | 1,445 | 1,415 | 30 |

| BUNKER PRICES | ||||

| 29 - Aug | 22 - Aug | CHG | ||

| RTM | 380cst | 397 | 406 | 9 |

| LSFO 0.50% | 480 | 461 | 19 |

|

| MGO | 647 | 649 | 2 |

|

|

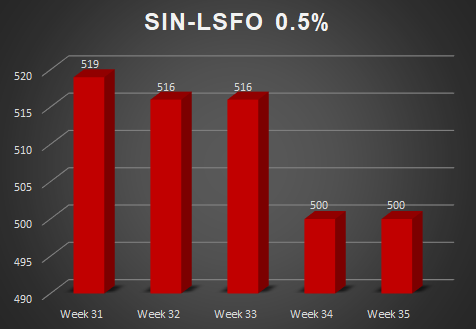

SGP |

380cst | 410 | 405 | 5 |

| LSFO 0.50% | 500 | 500 | 0 |

|

| MGO | 646 | 648 | 2 |

|

Tin nổi bật

-

-

Các nhóm cổ đông lớn tại Hải An

Ngày 10/09/2025

-

-

Thông báo về việc giao dịch chứng khoán thay đổi niêm yết

Ngày 29/08/2025

-

-

Quyết định thay đổi đăng ký niêm yết

Ngày 29/08/2025