Maritime Market News

News Highlights week: 50 - 2022

Ngày đăng: 19/12/2022 | Lượt xem: 738

Evergreen service to link Vietnam-Malaysia-Indonesia

Evergreen is set to organize next month a dedicated weekly service between Vietnam, Malaysia and Indonesia, aptly marketed as ‘VMI’. This upcoming service brand name is retaken from Evergreen’s previous ‘VMI’ loop that was originally launched in late 2011, linking Malaysia, Indonesia and Southern Vietnam.

This old ‘VMI’ ended in November 2018 with its final port calls, including Tanjung Pelepas, Port Kelang and Ho Chi Minh City, being covered by the revised ‘VSM’ loop at the time.

The new ‘VMI’ is scheduled to start with the 10 January sailing of the 1,844 teu EVER CHASTE from Haiphong. The loop will turn in three weeks with three ships of 1,800 – 2,000 teu calling at Haiphong, Ho Chi Minh City, Port Kelang (W), Tanjung Pelepas, Jakarta, Semarang, Surabaya, Singapore, Tanjung Pelepas, Haiphong.

Based on Alphaliner’s records, Evergreen will with this new 'VMI' become the second operator to offer a direct service between Northern Vietnam and Java island in Indonesia, adding to SITC, the only carrier currently serving this route.

ZIM adjusts China – Southeast Asia - Australia network

ZIM will later this month start to reshuffle its network of services between China, Southeast Asian countries and Australia.

The Israeli operator is expected to suspend two of its China – Australia services, the ‘CA2’, which links South China, Malaysia, Vietnam, Thailand and Eastern Australia, and the ‘C3A’, which connects North and Central China with Eastern Australia.

As part of the reshuffling, ZIM will introduce a new Vietnam – Thailand - Malaysia – Western and Eastern Australia service, dubbed ‘Thailand Fremantle Express’ (TFX) by the end of December. Gold Star Line will also be participating on this loop.

Besides covering parts of the Southeast Asia – Eastern Australia segment of the soon-to-be-suspended ‘CA2’, the ‘TFX’ will also provide ZIM with a new direct connection between Southeast Asia and Western Australia through a direct call at Fremantle.

Furthermore, while ZIM’s last China-Australia service, the 'CAX’, will remove Haiphong in Northern Vietnam later this month, the loop will as from next month add Nansha and Yantian.

> The new ‘TFX’ will turn in six weeks calling at Ho Chi Minh City (SPITC), Laem Chabang, Port Kelang (W), Sydney, Melbourne, Fremantle, Port Kelang (W), Ho Chi Minh City (SP-ITC). The service will kick off from Ho Chi Minh City with a sailing of the 2,553 teu GSL AFRICA. She will be joined by the 1,717 teu OPHELIA. The other ships are yet to be nominated.

Carrier volumes drop 5% but results vary across lines

A survey of liftings by Maersk, CMA CGM, COSCO, Hapag-Lloyd, OOCL, Yang Ming, HMM and ZIM shows the eight carriers moved a total of 71.08 Mteu in the first nine months of the year, a drop of 4.6% compared to the same period in 2021.

Among the individual carriers, the majority of lines saw a significant fall in volumes, with only Yang Ming, Hapag-Lloyd and CMA CGM managing to maintain levels so far over 2022.

Yang Ming was the sole carrier to report a significant increase, at 3.45 Mteu, a rise of 4.2% on the previous year. The Taiwanese carrier has benefited from a strong influx of new buildings in the same period, with 7 x 11,860 teu units delivered since October 2021, boosting its fleet capacity by more than 10% in the year to 30 September 2022.

CMA CGM and Hapag-Lloyd also reported stable volumes at the nine-month mark, at 16.59 Mteu and 8.98 Mteu respectively, unchanged on the same period in 2021.

The remaining five carriers surveyed each registered significant year-on-year volume declines for January-September: COSCO Shipping (excluding OOCL) was down -10.6%, Maersk –7.2%, HMM -7.0%, OOCL –6.2% and ZIM –2.5%.

Charter market ends 2022 weakened by the downturn, but things could be worse

The container charter market is ending 2022 in a very different mood from the euphoria of last year, at the same time. The severe market downturn of the middle of the year has taken its toll on charter rates which are today, on average, two-to-four times below their December 2021 level and even lower than that if compared to the historic rates reached in March 2022.

More than a correction, the market has suffered a proper crash, although it has come off from exceptionally (should we say abnormally?) high levels, entirely driven by the unprecedented Covid pandemic -related cargo boom.

Although the charter market has clearly fallen off a cliff, today’s charter rates remain twice as high as at the onset of the Covid pandemic. They are also, on average, much higher than during most of the 12 years preceding Covid, with the current level of the Alphaliner index being last reached in June 2008.

On the supply front, the situation for Non-Operating Owners (NOOs) is also much better today than it was before Covid, with only seven vessels currently in spot position, versus 76 in December 2019.

However, the market outlook is full of threats. On the supply side, the avalanche of newbuildings expected in 2023 and 2024, even with potentially delayed or cancelled orders will be hard to absorb if demand does not pick up substantially and scrapping rises sharply. Also, the numerous orders placed by carriers themselves will be detrimental to many NOO vessels which risk losing their employments.

On the demand side, the prospects of recession in many countries, a persistent multi decade-high inflation and continued geopolitical instability that keeps energy prices at record highs will continue to put a lid on commerce and container seaborne trade.

These negative factors will inevitably impact demand for container tonnage, with charter vessels first in line to bear the brunt of any fleet rationalizations by carriers

MKT

Chỉ số Thị trường

| EXCHANGE RATES | |||

| 22 - Aug | 15 - Aug | CHG | |

| $-VND | 26,520 | 26,450 |  70 70 |

| $-EURO | 0.862 | 0.855 | 7 |

| CNY-VND | 3,727 | 3,716 | 11 |

| SCFI | 1,415 | 1,460 | 45 |

| BUNKER PRICES | ||||

| 22 - Aug | 15 - Aug | CHG | ||

| RTM | 380cst | 450 | 449 | 1 |

| LSFO 0.50% | 508 | 507 | 1 |

|

| MGO | 719 | 741 | 22 |

|

|

SGP |

380cst | 420 | 415 | 5 |

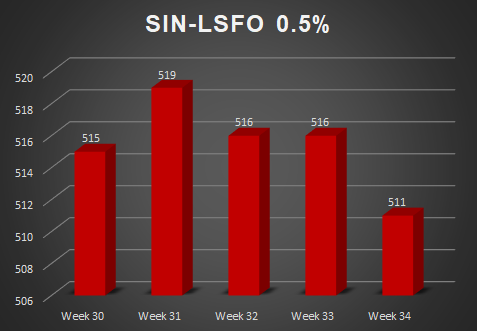

| LSFO 0.50% | 511 | 516 | 5 |

|

| MGO | 678 | 693 | 15 |

|

Tin nổi bật